How Quickly Will Premium Air Travel Return Amidst Continuing Pandemic Uncertainties?

As airlines fight for survival in a volatile, pandemic-scarred environment, real worries are emerging about when and how the all-important premium traffic will return.

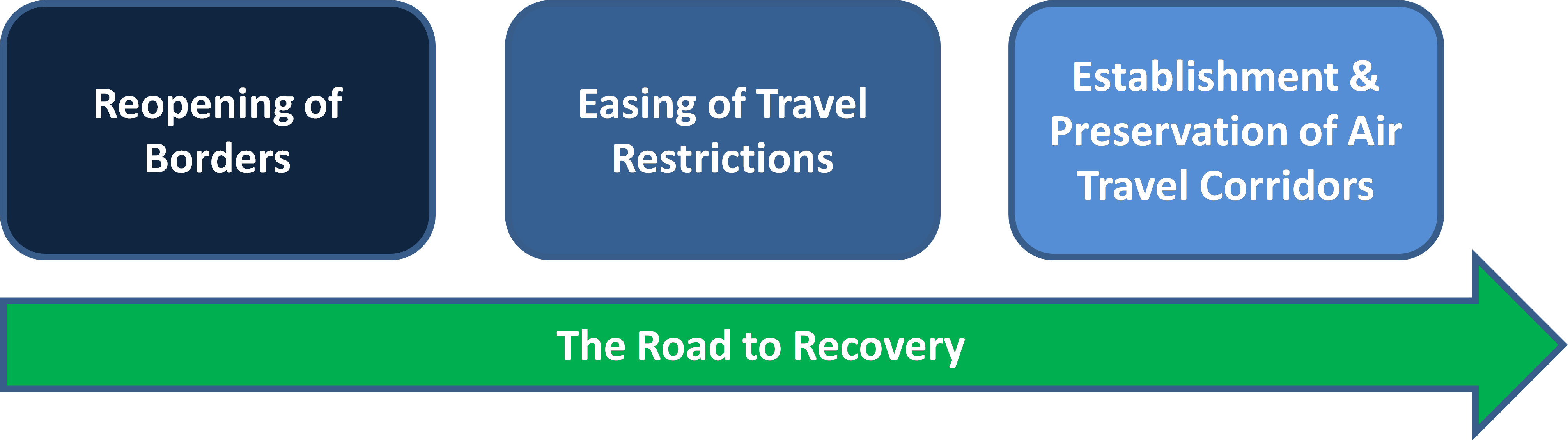

While the question of when premium traffic will make a comeback is something that is in the mind of every executive in airline boardrooms across the world, a more immediate question is what will it take for this all-important segment to take off again. Similar to leisure traffic, the underlying base requirements will be the same: reopening of borders, easing of travel restrictions, and preservation of air travel corridors.

However, these have proven to be difficult to implement and maintain in practice. The recent example of the UAE-UK air travel corridor has highlighted current fragilities. With the establishment of the air travel corridor on 12th November 2020, airlines immediately put their widely available capacity to serve the expected surge in demand. For example, Emirates re-established its links to the UK with multiple daily services to a range of UK airports, including London Heathrow, Manchester, and Birmingham. While not near its pre-pandemic flight schedules, the airline gradually increased capacity on these routes, including the utilization of its A380 fleet.

The glimmer of hope provided to airlines in this corridor along with other airlines in their respective corridors globally, however small within the global context, came to a grinding halt with the announcement of new lockdown measures by the UK Government on 5th February 2021. Despite having ample capacity available, this latest development presents significant uncertainty and planning challenges yet again for airlines.

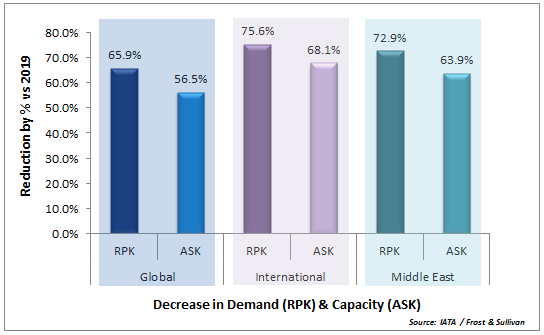

With the release of its 2020 full-year global passenger traffic results, IATA has confirmed what was already known within the industry: the industry is in dire straits, with 2020 officially the worst year in the history of air travel. With global passenger demand plunging by two-thirds compared to 2019, airlines have suffered extensively despite globally available capacity also shrinking by nearly 57% in the same period.

While domestic demand fared comparatively better with a decrease in demand just short of 49%, this provides little consolation for incumbent airlines of the Middle East. Particularly within the GCC, airlines are dependent on international demand, which declined by a disastrous 75.6%.

Even as the aviation industry struggles, it has become increasingly difficult to forecast when will the travel industry start to recover globally, be it for business or leisure. This has been and continues to be, due to the evolving challenges associated with global pandemic recovery efforts. Such challenges are presenting persistent road blocks to the steady recovery of global air travel, in particular to premium traffic that is the cornerstone of airline route and network profitability.

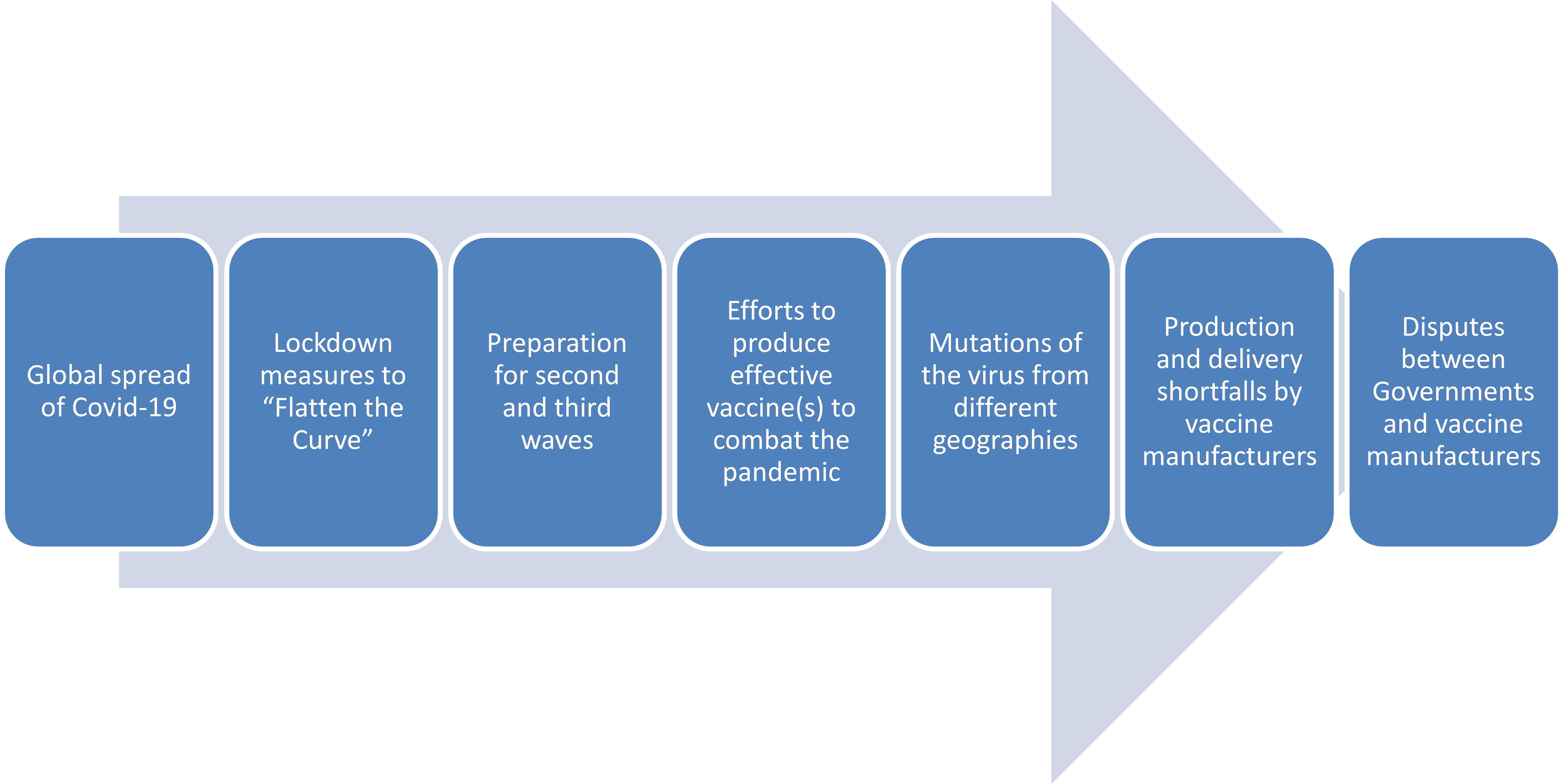

Business travel is expected to recover significantly more slowly than leisure travel, and even more slowly than previously recorded post-recession recoveries in air traffic experienced globally. Indeed, leisure traffic has always recovered faster than premium traffic following recessions caused by 9/11 or the 2008 global financial crisis. However, it is key to understand that these crises originated from one source and in this increasingly interconnected and globalized world, their impact was felt globally.

Today’s scenario is very different – not only is the world and its economies more interconnected than ever before, but we also have an ongoing global pandemic. Furthermore, the persistent lack of a truly globally coordinated approach to deal with the pandemic has meant that no two countries have been the same with regards to the spread of the pandemic, their response to it, or in the roll-out of their vaccination programs.

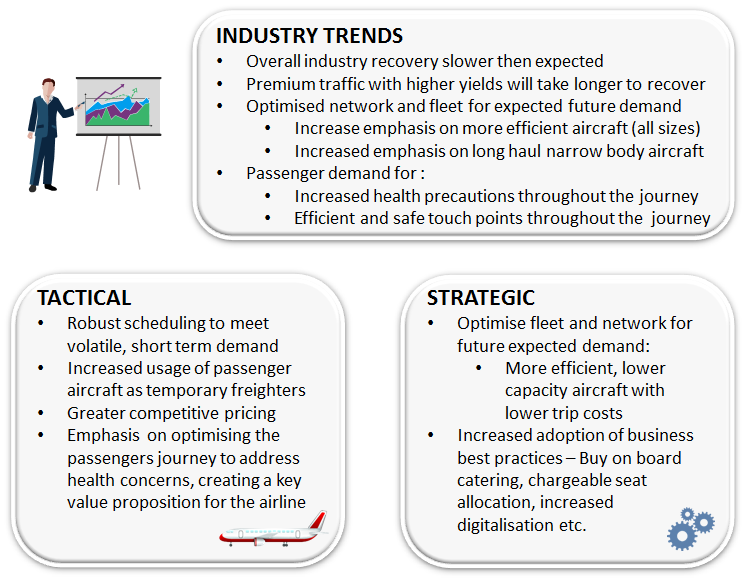

This will have distinct and substantial effects not only on changing trends within companies regarding corporate travel but also on the business models of a vast majority of airlines, going forward.

Corporate travel managers are likely to have additional concerns and a more complicated process flow when it comes to deciding and arranging travel for their employees. At a high level, these can be categorized as below:

With the overall absence of the crucially important premium traffic yields and unrelenting price competition from equally wounded competitors, the need to adapt and reinvent their business models is a clear and present fact for airlines.

In general, airlines face momentous challenges but only a limited arsenal with which to deal with them. With cash liquidity being the most important part of this arsenal, through strong cash reserves or governmental support during the crisis, airlines are limited in their ability to respond to such drastic changes in the market.

Consolidation of the industry is inevitable, with the size and shape of the consolidation depending on how long it will take to recover and achieve sustainable traffic levels globally. Airlines that can weather the storm will survive, others will look to merge or be acquired, while the remainder will face insolvency

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

__cfruid

session

This cookie is set by the provider Cloudflare. This cookie is used for load balancing and for identifying trusted web traffic.

_GRECAPTCHA

5 months 27 days

This cookie is set by Google. In addition to certain standard Google cookies, reCAPTCHA sets a necessary cookie (_GRECAPTCHA) when executed for the purpose of providing its risk analysis.

_PCCID

5 years

Identifies the visitor across devices and visits, in order to optimize the chat-box function on the website.

_PCCSID_363163

20 minutes

Required for functioning of the Pure Chat box.

cookielawinfo-checkbox-advertisement

1 year

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Advertisement".

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

JSESSIONID

past

Used by sites written in JSP. General purpose platform session cookies that are used to maintain users' state across page requests.

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Cookie

Duration

Description

__cf_bm

30 minutes

This cookie, set by Cloudflare, is used to support Cloudflare Bot Management.

aka_debug

session

This cookie is set by the provider Vimeo.This cookie is essential for the website to play video functionality. The cookie collects statistical information like how many times the video is displayed and what settings are used for playback.

bcookie

2 years

This cookie is set by linkedIn. The purpose of the cookie is to enable LinkedIn functionalities on the page.

lang

session

This cookie is used to store the language preferences of a user to serve up content in that stored language the next time user visit the website.

lidc

1 day

This cookie is set by LinkedIn and used for routing.

player

1 year

This cookie is used by Vimeo. This cookie is used to save the user's preferences when playing embedded videos from Vimeo.

vc

never

This cookie is set by addthis.com on sites that allow sharing on social media.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Cookie

Duration

Description

_gat

1 minute

This cookies is installed by Google Universal Analytics to throttle the request rate to limit the colllection of data on high traffic sites.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

_ga

2 years

This cookie is installed by Google Analytics. The cookie is used to calculate visitor, session, campaign data and keep track of site usage for the site's analytics report. The cookies store information anonymously and assign a randomly generated number to identify unique visitors.

_ga_6JHN0QW8FW

2 years

This cookie is installed by Google Analytics.

_gat_gtag_UA_197764616_1

1 minute

This cookie is set by Google and is used to distinguish users.

_gat_gtag_UA_53927943_3

1 minute

Set by Google to distinguish users.

_gd_session

4 hours

This cookie is used for collecting information on users visit to the website. It collects data such as total number of visits, average time spent on the website and the pages loaded.

_gd_svisitor

session

This cookie is set by the Google Analytics. This cookie is used for tracking the signup commissions via affiliate program.

_gd_visitor

2 years

This cookie is used for collecting information on the users visit such as number of visits, average time spent on the website and the pages loaded for displaying targeted ads.

_gid

1 day

This cookie is installed by Google Analytics. The cookie is used to store information of how visitors use a website and helps in creating an analytics report of how the website is doing. The data collected including the number visitors, the source where they have come from, and the pages visted in an anonymous form.

CONSENT

16 years 4 months 10 days 14 hours

These cookies are set via embedded youtube-videos. They register anonymous statistical data on for example how many times the video is displayed and what settings are used for playback.No sensitive data is collected unless you log in to your google account, in that case your choices are linked with your account, for example if you click “like” on a video.

vuid

2 years

This domain of this cookie is owned by Vimeo. This cookie is used by vimeo to collect tracking information. It sets a unique ID to embed videos to the website.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

bscookie

2 years

This cookie is a browser ID cookie set by Linked share Buttons and ad tags.

i

never

The purpose of the cookie is not known yet.

IDE

1 year 24 days

Used by Google DoubleClick and stores information about how the user uses the website and any other advertisement before visiting the website. This is used to present users with ads that are relevant to them according to the user profile.

test_cookie

15 minutes

This cookie is set by doubleclick.net. The purpose of the cookie is to determine if the user's browser supports cookies.

VISITOR_INFO1_LIVE

5 months 27 days

This cookie is set by Youtube. Used to track the information of the embedded YouTube videos on a website.

YSC

session

This cookies is set by Youtube and is used to track the views of embedded videos.

yt-remote-connected-devices

never

These cookies are set via embedded youtube-videos.

yt-remote-device-id

never

These cookies are set via embedded youtube-videos.

yt.innertube::nextId

never

These cookies are set via embedded youtube-videos.

yt.innertube::requests

never

These cookies are set via embedded youtube-videos.